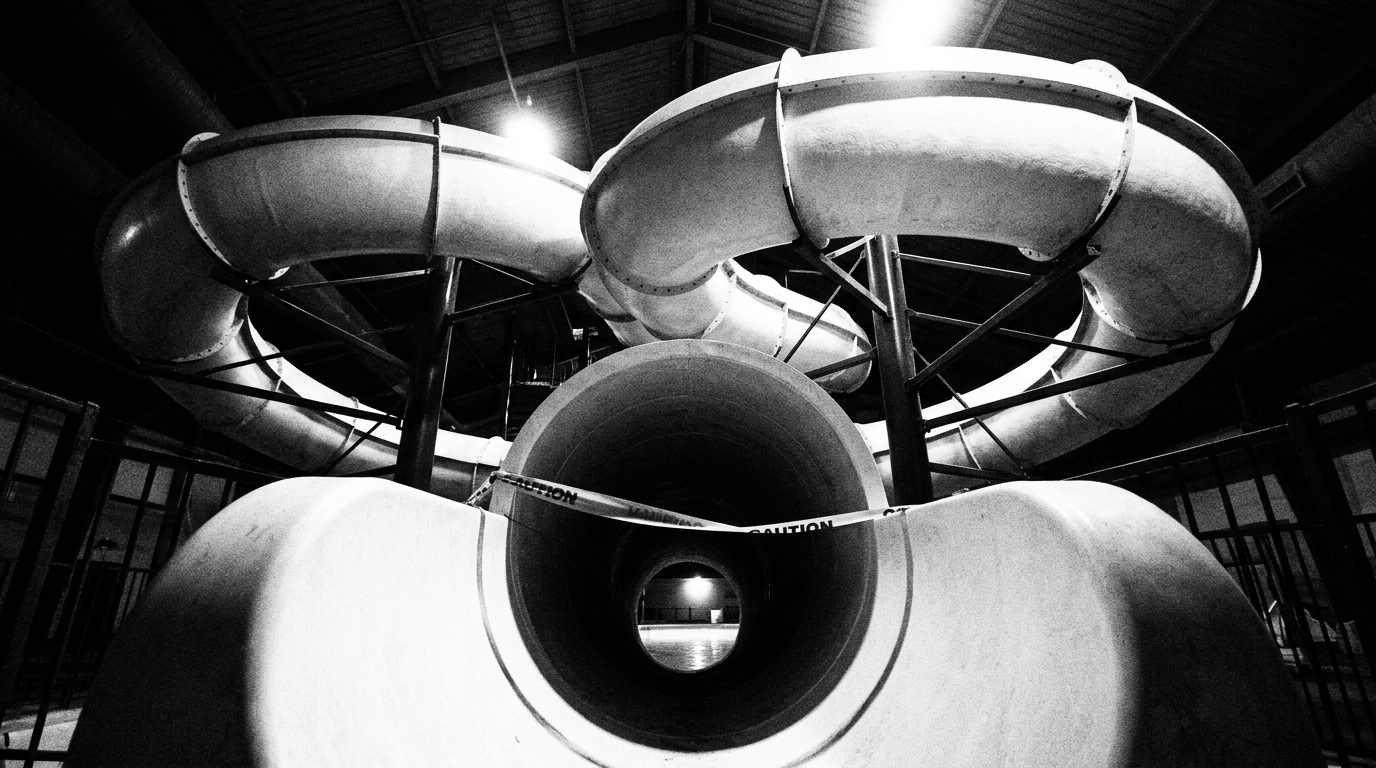

A Waterpark Hotel Ignored Health Inspectors for Two Months. Then the TV Cameras Showed Up.

A 114-key Holiday Inn in Omaha kept its waterpark running for over two months after the health department revoked its permits. It only closed when a reporter stuck a microphone in management's face. And if you think this is just an Omaha story, you haven't been paying attention.

Let me tell you what happened here, because the timeline is the whole story. December 2025, the Douglas County Health Department finds significant violations at this property's waterpark... wrong disinfectant system, pH levels out of range, low chlorine on the splash pad, loose handrails. They order it shut down. The hotel keeps operating. February 28th, Omaha PD issues a citation to the owner and all permits are officially revoked. The hotel keeps operating. March 4th, a KETV reporter shows up, does an on-camera interview with management, and less than an hour later... the pool closes.

Two months of defying a health department order. A police citation. Permits yanked. None of it mattered until a camera crew walked through the door.

I've seen this movie before. Not exactly this version, but close enough. I knew a GM once who inherited a pool with a cracked main drain cover. He flagged it to ownership, got told to "manage it" because the replacement part was $2,800 and they were in the middle of budget season. He shut the pool himself that afternoon. Called ownership back and said "I shut it down, the part's on order, and I'm not reopening it until it's installed. If you want to fire me for that, fire me." They didn't fire him. They bought the part. That's the difference between an operator who gets it and one who doesn't. The operator who gets it understands that the moment you KNOW about a safety issue and choose to keep operating, you've moved from "problem" to "liability." And the liability math is catastrophic.

Here's what nobody's talking about. The management company here, Avant Hotels, runs 11 properties in Nebraska. This isn't a rogue night manager making a bad call. This is an organizational decision to continue operating an attraction that the county health department said was unsafe. For two months. That's not a mistake. That's a strategy... one that bet the PR wouldn't catch up before they could fix things on their own timeline. And the strategy worked, right up until it didn't. The operator claims they addressed the issues in December and documented water quality every four hours. The health department says the pool was operating illegally the entire time. Both of those things cannot be true.

And where was the brand? KETV reached out to IHG. No comment. Look... I understand the franchise model. IHG doesn't operate this hotel. But their name is on the building. Their loyalty members are swimming in that pool (or were, for two months, while the permits were revoked). Every franchisor has quality assurance processes, inspection protocols, standards enforcement mechanisms. This property has "Waterpark" literally IN its hotel name under the IHG flag. At some point, the brand has to answer for what happens under its sign, or the sign means nothing. If you're an owner paying 15-20% of revenue in total brand costs, part of what you're buying is the assurance that the brand protects its own reputation. When the brand goes silent on something like this, every franchisee in the system should be asking what they're actually paying for.

This is a 114-key property in a market that's already softening... Omaha saw occupancy and ADR both decline year-over-year as of late 2025, with RevPAR down roughly 4%. There's a 100,000 square foot indoor waterpark opening about 20 minutes away in early 2027. And this isn't even the first time Omaha's had a waterpark hotel shut down by health inspectors... a different property at a Ramada got hit with the same thing back in 2018. The pattern is clear. Waterpark amenities in hotel properties are operationally complex, maintenance-intensive, and regulated differently than a standard pool. If you're running one (or your owner is thinking about adding one), the compliance infrastructure has to be treated like life safety, not like an amenity upgrade. Because when it goes wrong, it doesn't go wrong quietly. It goes wrong on the evening news.

If you operate a property with any aquatic amenity... pool, splash pad, waterpark, whatever... pull your compliance file this week. Confirm every permit is current, every inspection is documented, every chemical log is up to date. If something's out of compliance, shut it down TODAY, not when someone makes you. The math on this is simple: a closed pool costs you some guest complaints and maybe a few refunds. An open pool that shouldn't be open costs you your franchise agreement, your insurance coverage, and potentially your entire business. And if your owner pushes back on the cost of compliance, remind them that this Omaha property just became a national news story. That kind of exposure doesn't wash off with a press release.